Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Intel stock (NYSE: INTC) rose sharply yesterday after the company began laying off employees from its Oregon plant. However, analysts are cautious about the company despite the company aggressively working on a turnaround under CEO Lip-Bu Tan.

Intel would lay off around 500 employees from the Oregon plant, which is part of the previously planned reduction in its global workforce. The company laid off around 15,000 employees last year, which was the biggest in its history, and has guided for more cuts. “There is no way around the fact that these critical changes will reduce the size of our workforce,” Tan said in a memo to employees earlier this year.

Intel is undergoing a significant corporate restructuring strategy that includes global layoffs to streamline operations, cut costs, and boost efficiency. This effort is aimed at making the company leaner and more competitive in the fast-changing semiconductor market. The measures have generally been received positively by the markets as they are seen as a necessary step for Intel to regain its footing.

Citi is Cautiously Optimistic on INTC Stock

Analysts are cautious on Intel and most rate the stock as a hold. Citigroup recently raised its price target on Intel to $24 from $21, citing “cautious optimism” around the company’s transformation plans under its Tan. However, in its note, the brokerage noted that Intel’s share of global chip shipments fell to 65.3% in Q1 2025, down 1.8% sequentially and the lowest level since it began tracking the industry in 2002.

Intel was quite slow with innovation, and AMD gradually took its market share in the PC market. Apple, too, stopped using Intel chips for its Mac and instead pivoted to its own chips.

Intel’s woes are far from over, and Nvidia, AMD, and Qualcomm are looking to further eat into its PC market share with Arm-based semiconductors. Intel is still working with its x86 technology, which it created in 1981.

More recently, Intel seems to have lost out on the race in artificial intelligence (AI) chips, even as rivals, especially Nvidia, are printing money selling AI chips.

Intel Is Working on a Turnaround

Tan, meanwhile, is working on a long-term plan to turn around Intel and outlined the strategy during the recent earnings call. Firstly, he said that the company will focus on product development, stressing “best products always win.”

Secondly, he said that Intel will “refine” its AI strategy. “Our goal will be to take our integrated system and platform view to develop full stack AI solutions that enable more accuracy, power efficiency and security for our enterprise customers,” said Tan during the earnings call.

Thirdly, he talked about “building trust with foundry customers.” Gelsinger had big plans for Intel’s foundry business, but that segment has sagged and has been saddled with billions of dollars in losses.

Finally, he said that Intel will strengthen its balance sheet. He, however, said that the company has decided not to “spin off Intel Capital, but to work with the team to monetize our existing portfolio while being more selective on new investments that support the strategy.”

Intel Reported Better Than Expected Q1 Earnings

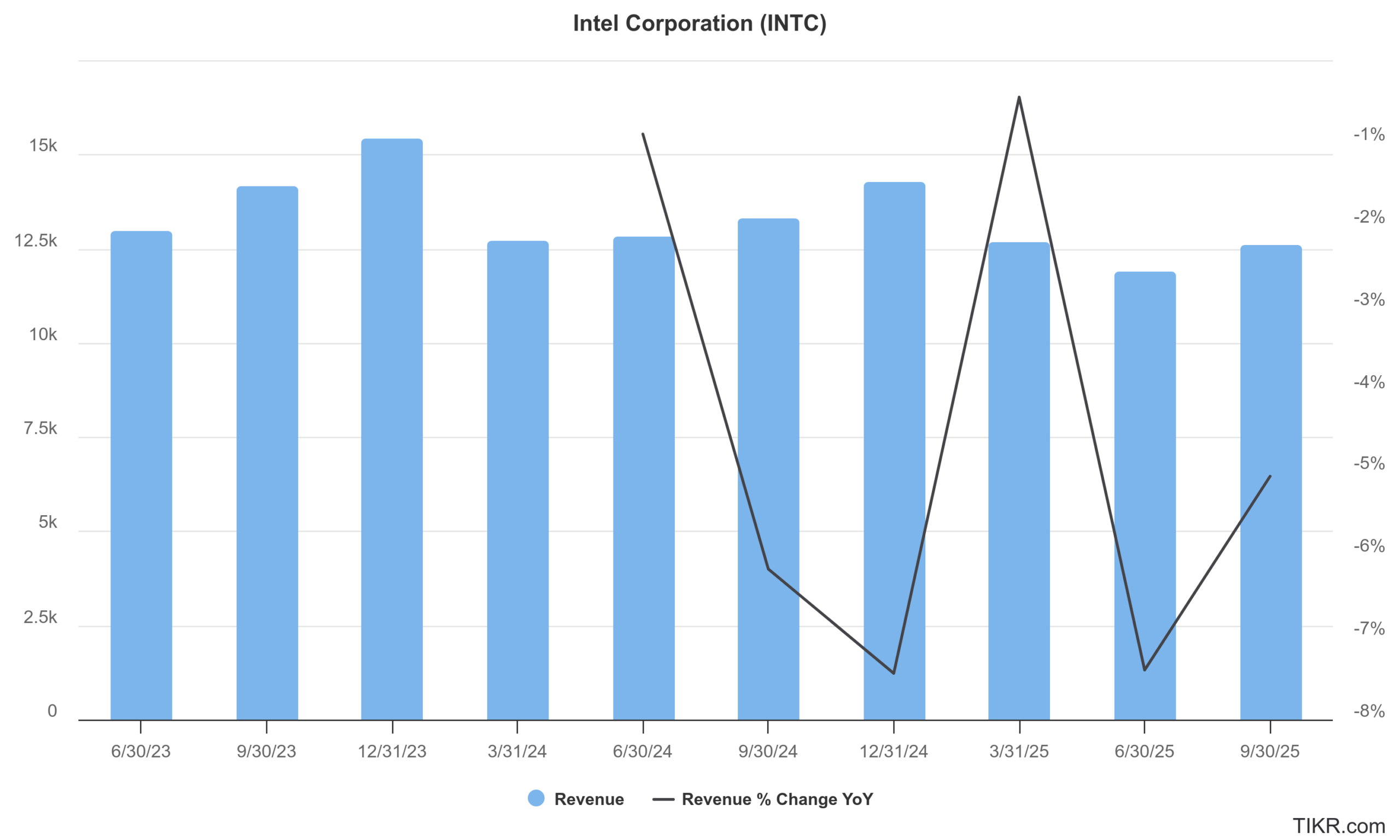

Intel reported revenues of $12.7 billion in the first quarter, which was similar to the corresponding quarter last year. The company’s sales, however, easily surpassed the $12.3 billion that analysts were expecting. Intel reported an adjusted EPS of 13 cents, which was also ahead of the 1 cent that analysts were modelling. The company, however, posted a GAAP per-share loss of 19 cents.

Meanwhile, while Intel’s Q1 earnings were better than feared, the company’s Q2 guidance spooked investors. It forecast revenues between $11.2 billion-$12.4 billion in the current quarter, which CFO David Zinsner admitted was “wider than normal” due to the uncertainty over tariffs.

Amid a tough macro environment, Intel is looking to slash its capex as well as operating expenses. The company has slashed its 2025 capex target by $2 billion to $18 billion while lowering the operational expenses target from $17.5 billion to $17 billion. The company is looking to cut its operational expenses by another $1 billion in 2026.

Intel Will Release Its Q2 Earnings Later This Month

Intel will release its Q2 earnings later this month. The most significant factor will be tangible evidence of cost savings from the ongoing global layoffs and operational streamlining. Tan’s vision of a “leaner, meaner” Intel hinges on reducing operating expenses. Any signs that these efforts are translating into improved margins will be highly scrutinized.

Intel has been investing heavily in AI-enabled processors, but has faced weaker-than-expected demand for these chips, with consumers often opting for older, more affordable models. The Q2 report will provide insights into the performance of its newer architectures and market acceptance.

Investors will also watch out for commentary on the foundry business, which has been burning cash. There have previously been reports that Intel is looking to sell that business. However, none of the rumors came to fruition.

INTC Is at a Crucial Juncture

Intel’s guidance for the third quarter and the remainder of 2025 will be critical. Any upward revisions, even modest ones, would signal growing confidence in its turnaround. Conversely, further cautious guidance could dampen investor enthusiasm.

Intel is at a critical juncture. After years of struggling with manufacturing delays and fierce competition from AMD, the company is undertaking a massive transformation. The Q2 earnings report will not just be about numbers; it will be a crucial progress report on Intel’s journey to reclaim its technological leadership and financial strength in the global semiconductor industry. Investors will be looking for concrete signs that the ship is indeed turning.

#Intel #Stock #Rises #Layoff #News #Analysts #Stay #Cautious